How the 2025 “One Big Beautiful Bill” Impacts Real Estate Taxes for Homeowners, Investors, and Developers

- sonya9686

- Aug 8, 2025

- 11 min read

Introduction:

The One Big Beautiful Bill Act of 2025 (H.R. 1) is a sweeping federal tax law, championed by President Donald Trump and House Republicans, that has officially been enacted. Introduced in the House in May 2025 and passed by both chambers (House on May 22, Senate on July 1), this significant legislation was signed into law by President Trump on July 4, 2025, becoming Public Law No: 119-21. It extends many 2017 tax cuts and introduces new incentives aimed at stimulating investment across various sectors. Real estate stakeholders – from homeowners to investors and developers – have a lot to gain (and plan for) under the bill’s provisions. Below, we break down the key tax changes and what they mean for you.

Prefer to watch instead?

I also break down these tax changes in a quick YouTube video — covering what the One Big Beautiful Bill means for homeowners, investors, and developers.

Impact on Homeowners

For American homeowners, the new law provides several forms of tax relief and certainty:

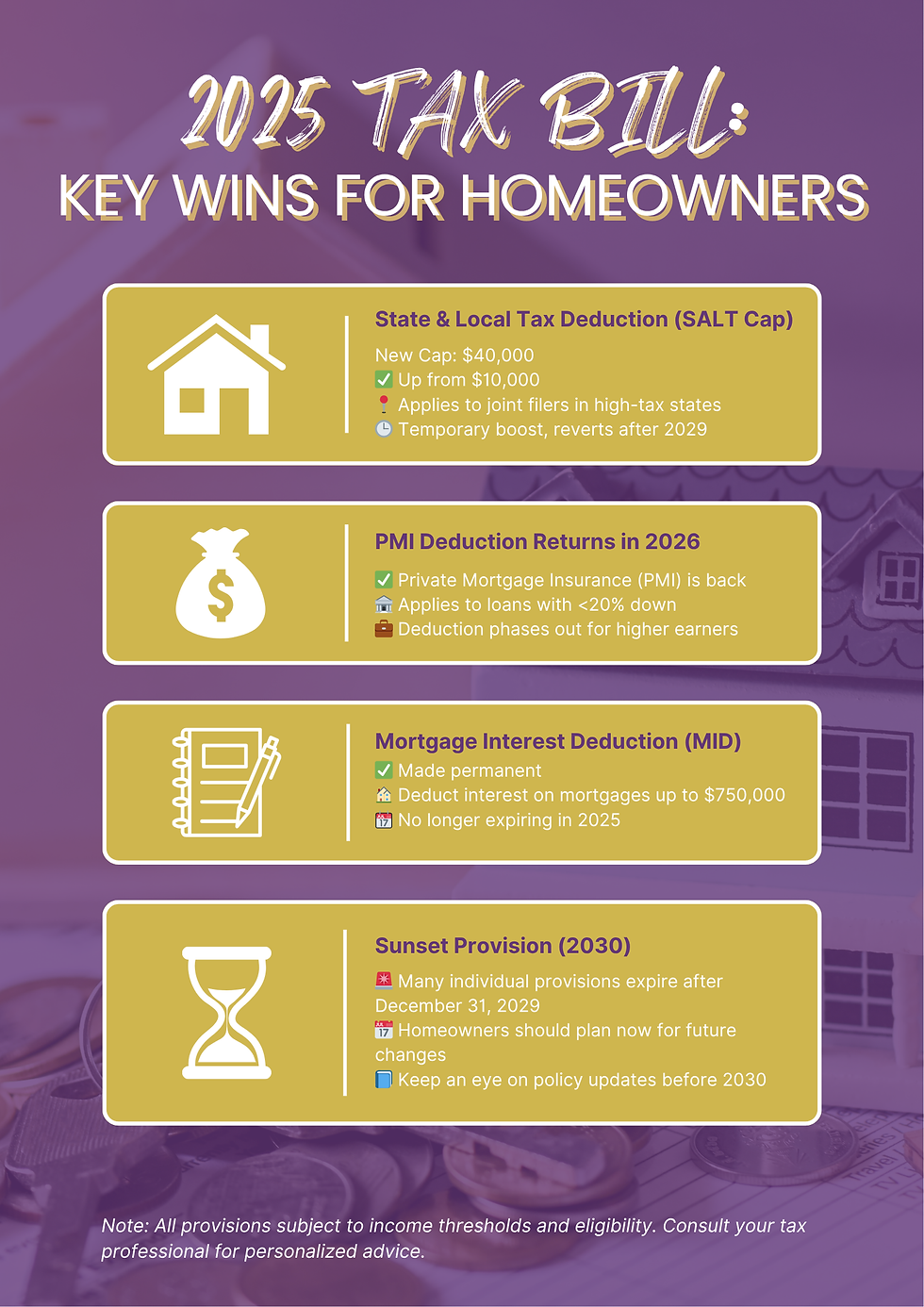

State and Local Tax (SALT) Deduction Relief: The cap on SALT deductions (state income and property taxes) increases from $10,000 to $40,000 for 2025, offering significant relief, especially to those in high-tax states. This expanded cap will adjust by 1% annually through 2029, then revert to $10,000 in 2030, due to a built-in sunset provision. (Incomes above $500,000 face a partial phase-out of this expanded deduction.) Homeowners in high-tax states will benefit in the short term, though critics note this predominantly helps higher earners and is a temporary reprieve.

Mortgage Interest Deduction (MID): The mortgage interest deduction rules from the 2017 tax law are now made permanent. Homeowners can continue to deduct interest on up to $750,000 of mortgage debt (or $375,000 for single filers) on primary and secondary homes. This means the previous higher $1 million debt limit will not return after 2025. The law also solidifies the rule that interest on home equity loans is only deductible if the loan was used to buy, build, or substantially improve the home; interest on equity loans used for personal expenses remains non-deductible permanently. By keeping the lower debt cap and home-equity limits, the bill continues to target tax benefits toward middle-class and first-time buyers in expensive markets, while limiting subsidies for ultra-high-value mortgages.

Mortgage Insurance Premiums (PMI/MIP) Deduction: In a win for new and moderate-income homeowners, the ability to deduct mortgage insurance premiums is restored. Starting in 2026, borrowers who pay private mortgage insurance (PMI) or FHA mortgage insurance premiums can once again treat those premiums as itemized deductions. This tax break had expired after 2021; its return means many first-time buyers with lower down payments will receive extra tax relief. By including PMI/MIP in deductible housing costs, the law makes it more feasible for buyers with less equity to itemize deductions and save on taxes. (Note: Income phase-outs may apply, as under prior law.)

Takeaway for Homeowners: The OBB Act’s homeowner provisions can lower tax bills for those with significant state/local taxes or mortgage costs. If you’re in a high-tax state or bought a home with a small down payment, you could see greater deductions in coming years. However, remember that the SALT relief is temporary – maximize it before 2030. All homeowners should evaluate whether itemizing deductions now yields more benefit given these expanded write-offs.

Impact on Real Estate Investors

Real estate investors – owners of rental properties, passthrough entities, and others with real estate businesses – benefit from several favorable tax changes under the new law:

100% Depreciation (Bonus Depreciation) Extended: The bill extends 100% bonus depreciation for qualifying property and equipment. Under prior law, bonus depreciation was phasing down from 100% to 0% by 2027, but now investors can continue to immediately write off the full cost of depreciable assets like appliances, machinery, and qualified improvement property in the year of purchase. For example, if you purchase new appliances or make qualifying improvements in an apartment building, you can deduct the entire cost right away rather than depreciating over many years. This full expensing is a major tax saver that encourages reinvestment into properties and upgrades. (Note: Land and building structures generally are not eligible for bonus depreciation, except for certain short-lived structures under a temporary provision related to Qualified Production Property.)

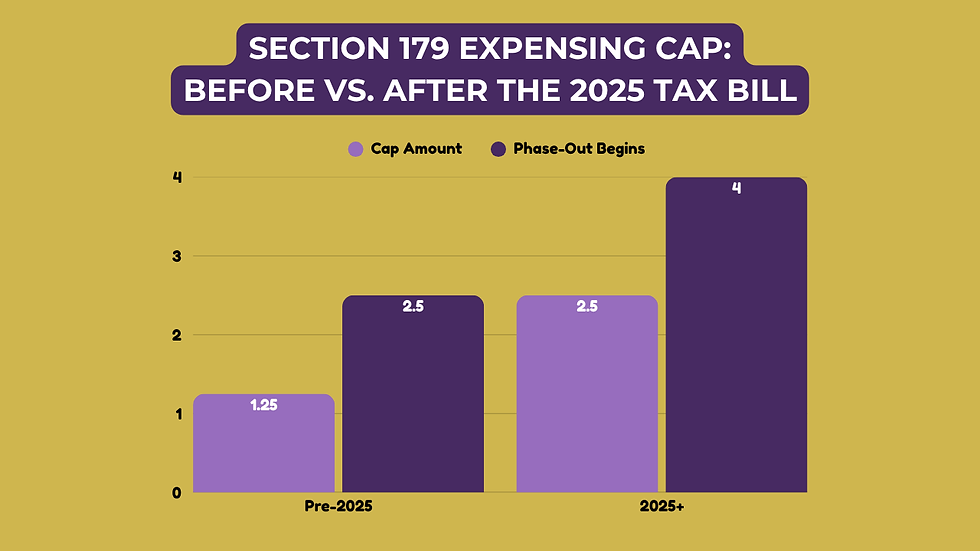

Expanded Section 179 Expensing: In addition to bonus depreciation, Section 179 expensing limits are significantly increased. The maximum deduction for business property purchases under Section 179 jumps to $2.5 million (from $1.25 million), with the phase-out threshold increased to $4 million of purchases, effective 2025. This change, made permanent and indexed for inflation, benefits investors in small to mid-sized real estate businesses (such as those purchasing equipment, furniture, or light vehicles for property management or development). It substantially raises the ceiling before a business hits the cap on immediate expensing, meaning even more of your capital investments can be deducted upfront rather than depreciated. Together, bonus depreciation and expanded §179 expensing improve cash flow and ROI on property improvements and equipment.

Looser Limits on Business Interest Deductions: The Act locks in a more generous rule for deducting business interest on loans temporarily for tax years 2025 through 2029. It sets the limit at 30% of EBITDA (earnings before interest, taxes, depreciation, and amortization), instead of the stricter EBIT-based limit that was scheduled to take effect. Under prior law, starting in 2022, the deduction for interest expense was to be capped at 30% of EBIT (which excludes depreciation/amortization), significantly reducing deductible interest for heavily leveraged real estate companies. By using EBITDA for this period, the law allows more interest to be written off each year. Real estate investors who borrow to finance properties will be less likely to hit the interest limitation during these years. (Many real estate businesses were exempt by electing out with longer depreciation, but now more can deduct interest without those trade-offs.) Bottom line: the cost of borrowing to buy or improve property stays more tax-efficient, supporting leverage as a tool for growth.

Section 199A Pass-Through Deduction Made Permanent: Investors operating through LLCs, partnerships, S-corporations or sole proprietorships continue to benefit from the 20% Qualified Business Income (QBI) deduction beyond 2025. The new law makes the Section 199A deduction for pass-through business income permanent, whereas it was slated to expire after 2025. Additionally, the income thresholds for phasing out this deduction are increased – for joint filers, the phase-out now begins at $150,000 of income (up from $100,000) starting in 2026. This means more real estate professionals (who often report rental income or REIT dividends qualifying for QBI treatment) can claim the full 20% write-off on their business income. Preserving this deduction encourages investors to maintain pass-through ownership structures and rewards ongoing real estate enterprise with lower effective tax rates. Be mindful of the rules (like meeting the IRS safe harbor for rental real estate enterprises to count as a business), but know that this valuable tax break is here to stay.

Opportunity Zones – Extended and Enhanced: One of the most significant boosts for investors is the overhaul of the Qualified Opportunity Zone (QOZ) program. Originally set to stop accepting new investments after 2026, the program is now extended indefinitely with rolling designations of zones. Every 10 years starting in 2026, states can nominate new economically distressed areas as Opportunity Zones, keeping this incentive fresh for directing capital to underserved communities. Key improvements include a rolling 5-year deferral for reinvested capital gains (replacing the old fixed 2026 end-date) – any capital gain you roll into a Qualified Opportunity Fund can now be deferred for five years from the investment date, no matter when the gain arose. After that 5-year period, 10% of the deferred gain is forgiven via a stepped-up basis (essentially a 10% tax reduction on the original gain). The law makes this 10% exclusion permanent, though it did eliminate the previous additional 5% bonus for seven-year holds. Crucially, the signature tax-free growth feature remains: if your Opportunity Zone investment is held for at least 10 years, any appreciation (gain) on that investment can be realized 100% tax-free. Investors thus continue to have a powerful vehicle for sheltering both initial gains and long-term profits.

Furthermore, the revised program tightens zone eligibility to ensure investments target true low-income areas (using stricter income tests and ending the inclusion of high-income “contiguous” tracts). It also introduces special “Qualified Rural Opportunity Funds” that invest in rural zones, offering enhanced tax benefits such as potentially a higher basis step-up after 5 years (e.g., 30% versus 10% for typical zones). For real estate investors, the upshot is a longer and more impactful Opportunity Zone program: you have ongoing chances to defer and reduce taxable gains by investing in designated communities, with larger incentives for rural development. With no looming 2026 cutoff, there’s more flexibility in timing these investments – but also new reporting requirements to mind, as transparency is increased.

Takeaway for Investors: The tax landscape for real estate investors remains very favorable. The ability to immediately write off property improvements and equipment costs (100% expensing) and to fully deduct most interest expense (for a temporary period) can significantly boost after-tax returns on new projects or capital upgrades. Meanwhile, the continuation of the 20% pass-through deduction locks in a lower tax rate on your rental or business income for the long haul. Perhaps most exciting, the Opportunity Zone program is now a permanent part of the tax code – offering a mix of deferral, partial forgiveness, and tax-free growth on invested gains. Investors should consider how these incentives might factor into their strategies: for example, accelerating planned capital expenditures to take advantage of full expensing, or rolling this year’s property sale gains into an Opportunity Zone fund to diversify and defer taxes. Always consult with a tax advisor to navigate the qualification details, but overall the climate for real estate investment and development just became even more tax-friendly.

Impact on Developers and Builders

Property developers, homebuilders, and investors involved in real estate development will see benefits aimed at spurring more construction – particularly for housing – and lowering the after-tax cost of projects:

Low-Income Housing Tax Credit (LIHTC) Expansion: In a bid to address affordable housing shortages, the One Big Beautiful Bill Act significantly expands the LIHTC program. Starting in 2026, the annual allocation of 9% housing tax credits to each state will permanently increase by 12%, meaning states get more credits to award to affordable rental housing projects. Importantly, for the 4% “bond-financed” LIHTC projects, the private-activity bond financing requirement is reduced from 50% to 25% of project costs. This “25% test” makes it much easier for developments to use tax-exempt bonds and qualify for 4% credits, effectively enabling more projects to get funded with less bond volume. These changes, drawn from the bipartisan Affordable Housing Credit Improvement Act, are projected by some analysts to add about 1.0 to 1.3 million additional affordable housing units nationwide over the next decade. For developers specializing in affordable housing, the boost means more deals will pencil out: smaller projects can access credits, and states will be able to approve a greater number of developments or deeper subsidies. Even market-rate developers might benefit indirectly, as expanded LIHTC could relieve some pressure in low-income segments or open up opportunities to partner on mixed-income projects. This is a clear win for the housing industry’s capacity to produce below-market rentals, though it comes as part of a trade-off (the bill cuts certain HUD green retrofit funds elsewhere).

Bonus Depreciation for Building Improvements: Developers can take advantage of the 100% bonus depreciation on eligible property, just as investors can. While land and new buildings generally must be depreciated over 27.5 or 39 years, many components of a development qualify as personal property or land improvements with shorter lives (think machinery, equipment, landscaping, appliances in units, etc.). Under the extended full expensing provision, a developer can immediately write off all costs for qualifying assets in a new construction or renovation project – for instance, installing $500,000 worth of new HVAC and security systems in an apartment complex could yield a $500,000 first-year deduction instead of being depreciated over decades. The law even added a temporary 100% cost recovery for certain structural components (like some non-residential structures) placed in service in the next few years, specifically for Qualified Production Property. The bottom line: if you’re developing property, the tax code now incentivizes front-loading your investment in project infrastructure and equipment by offering immediate expensing – effectively lowering the after-tax cost of development.

Section 179 Expansion for Business Assets: The doubling of Section 179 expensing limits (to $2.5M) is particularly useful for small and mid-size developers and contractors. Many of the tools, computers, vehicles, and office fixtures that a development firm purchases can be expensed under §179. With a higher ceiling, even outfitting a new office or buying construction equipment is less likely to hit the cap. For example, a homebuilder who buys $1.5 million worth of new construction machinery in 2025 can elect to expense the entire amount under §179 (whereas under old limits only about $1.25M would have been immediately deductible). This provision complements bonus depreciation and is especially valuable for those who may lease rather than own real estate (since §179 can be used on a broad range of tangible business property, including certain improvements to nonresidential buildings). The result is increased cash flow and simplified accounting for capital expenditures, benefiting developers investing in their business operations.

Other Housing-Related Tax Credits and Incentives: The Act’s focus was largely on extending existing incentives rather than introducing brand-new ones, but there are a few notable mentions:

The New Markets Tax Credit (NMTC), while not housing-specific, was made permanent as well. This credit can support mixed-use developments in low-income communities (e.g., a project with retail or community facilities alongside housing). Developers working in urban revitalization may find more stable financing opportunities with NMTCs now an ongoing program.

On the flip side, some energy-efficiency credits for housing were rolled back. The law repeals the recently expanded Energy Efficient Home Credit (45L) after one year, and ends homeowner energy improvement credits (25C, 25D) after a short phase-out (terminating after December 31, 2025, for many provisions). Builders had used the 45L credit (worth up to $5,000 per new efficient home) as a subsidy for green building; going forward, that incentive will vanish unless renewed separately. Developers should be aware that while core real estate tax benefits are enhanced, some green building incentives have been withdrawn under this bill’s cost-cutting measures.

What to do next?

The 2025 One Big Beautiful Bill Act ushers in a host of real-estate-friendly tax provisions: homeowners get a (temporary) break on SALT and a boost to deductible housing costs; investors and landlords see their favorite tax cuts extended and even enriched; and developers find more support for building via tax credits and write-offs. It’s a complex law, and not every change is permanent, so it’s crucial to understand the timelines and plan around them.

What should you do now? First, evaluate your tax position in light of these changes. Homeowners who previously hit the SALT cap or paid mortgage insurance should revisit whether itemizing deductions makes sense from 2025 onward. Investors should consider accelerating improvements or acquisitions to utilize 100% expensing and ensure they maintain compliance to claim the 20% QBI deduction in future years. Those with large capital gains might explore Opportunity Zone funds under the new rules to defer and reduce taxes. Developers and builders, check your project pipeline: affordable housing deals might now pencil out with the richer LIHTC, and any planned equipment purchases or build-outs could yield immediate tax savings if timed right.

As always, consult with a tax professional who understands real estate. The changes are nationally focused, but your individual strategy should be tailored: for example, high-income taxpayers might face new itemized deduction limits that require planning. Tax laws can also evolve – what’s given temporarily (like the SALT relief) could disappear, and future legislation could tweak these rules further. For now, real estate professionals and property owners have a prime window to maximize tax benefits. By staying informed and proactive, you can use the One Big Beautiful Bill’s incentives to your advantage – lowering your tax liability and reinvesting the savings in your portfolio and communities.

Sources:

This overview is based on analyses and summaries of the enacted One Big Beautiful Bill Act (H.R. 1, Public Law No: 119-21) provided by reputable organizations, including the Bipartisan Policy Center, Cherry Bekaert, Duane Morris LLP, Gulf Coast Business Law Blog, McGuireWoods LLP, Parker Poe, Williams Mullen, and others. Always refer to official IRS guidance and consult your tax advisor for specifics on applying these tax rules to your situation.

Comments